BYDDY // Blue 2 // Strike Price = {subscribe}

- 10 year CAGR = 25.9% (historical stock results Apr 11, 2013 to Apr 11, 2023)

- Future Growth Rate Estimate: {subscribe} (based on our analysis of past financial results, qualitative research, and Analyst estimates of future revenue and earnings)

- 5 year Price Target = {subscribe}

// WHY BUY

BYD isn’t the next Ferrari or Mercedes. It is the next Toyota Corolla because Toyota refused to electrify theirs. Japanese car manufacturers were once scrappy startups but eventually became behemoths. That process is repeating. Corolla, meet Dolphin. BYD isn’t made in China crap, it is the mix of quality, price and reliability that sells a crapload of cars to the masses. First they take China, then the rest of Asia, Europe and the Southern Hemisphere. They still haven’t figured out how to take the US, but they will. They already produce (in Lancaster, California) and sell buses and things in NA.

China leads the world in BEV sales and BYD is the dominant player in China: 179.5K sales in the first two months of 2022 up 76% to 316.5K in 2023. Even Tesla isn’t growing that rapidly, up 43% with 42.5K vs 60.7K in that time frame.

BYD started out as a battery maker. This production capability gives them cost advantages seeing as batteries are the primary cost factor of an EV as the rest is essentially all about window-dressing. Even Tesla buys batteries from BYD. Their LFP blade batteries are the best when it comes to the mix of range, cost, performance and reliability. And BYD appears to be innovative when it comes to battery development as they pioneer the transitions to batteries that include sodium in place of lithium. They are the world’s second largest battery producer behind CATL.

The thing holding the stock back is the China factor. It’s difficult for non-Chinese investors to trust that the CPC isn’t going to do something that will destroy this investment for us foreign bag-holders. However, BYD is a flagship company for the CPC. Arguably THE flagship company. How can you present yourself as a real playa on the world stage without a globally important auto manufacturer. Face unsaved without BYD, we might suggest. But the China factor will hamper the stock price and may stop it from ever getting a premium valuation like Tesla even though it is growing faster than Tesla at this point. In terms of car production – not in terms of mega-projects like Tesla is engaged in (e.g. humanoid robots).

Our Strike Price and price projections are throttled 50% because of the China factor, but this is a crucial company to know about if you like EVs. Even Buffett+Munger invested in BYD. In 2008 shockingly. When BYD was a mere child (company was formed in 1995).

// ChatGPT: WHY BUY … ?

If you are interested in BYD stock, it might be because BYD is a Chinese multinational company that specializes in automobiles, rechargeable batteries, and other green energy technologies. They are known for their electric vehicles and are considered one of the leaders in the EV industry in China. The company has been growing rapidly in recent years, with its stock price experiencing significant gains.

BYD has also been expanding its global reach and has formed partnerships with various international companies to manufacture and distribute its products. In addition, the company has received attention from investors and policymakers due to its focus on sustainable energy and environmental protection.

// CONCLUSION

They don’t have Tesla margins yet; 5% vs 17% operating margins. But unlike all other EV makers (ex-Tesla), BYD actually makes money selling EVs. In 2022 they made 1.85M units and about half were fully electric and half hybrid or ICE. Unlike legacy auto manufacturer’s who only have an EV ratio of 10% or less, BYD will be able to rapidly pivot to fully electric production. BYD shares Tesla’s vertical integration strategy which also makes them more nimble than legacy competitors. BYD has a very low price-revenue ratio of 1.6. Tesla is 7.7. BYDs FCF yield is 3.7% vs only 1.6% for Tesla. Their debt to assets ratio is even. In the long-run Tesla will be the bigger company, but in the meantime if BYD ever gets priced like the growth company it is (albeit more hardware than software), then the stock could move up multiples.

// CATALYSTS

Keith Williams: “The next phase of China’s emissions reduction regulations [China 6], due July 1, 2023, might mean millions of petrol and diesel cars will no longer be able to be sold in China.” Add this to Na replacing/augmenting Li and LFP going LMZAP “resulting in 210 Wh/kg energy density” and “expect the era of cheap BEVs to be very close.”

BYD moving to sodium-ion batteries starting Q2 2023, including in the Qin, Dolphin and Seagull. In China, Seagull is reported to be as cheap as $8,860.

BYD is expected to become the world’s largest BEV manufacturer in 2023 despite no sales in the US. Yet. But they have big plans in Asia, Europe, etc.

BYD is starting to lead the pace of change in batteries and EVs.

// RISKS

China factor. Competition.

// NEWS & COMMENTS

Apr 5, 2023

SA // buy: BYD And New Batteries: Cheap BEVs Coming, And Don’t Forget Tesla

I’m now convinced that this year might be the year when it becomes clear that we are entering the end of the ICE. Three companies have a leading role in this transition. They are Chinese companies CATL (Contemporary Amperex Technology Co (300750.SZ)), which is the dominant lithium battery manufacturer and innovator, and BYD (OTCPK:BYDDF) the second leading battery maker, but also a major electric automobile, truck and bus manufacturer. The third key company is Tesla (TSLA).

// GGI 💬

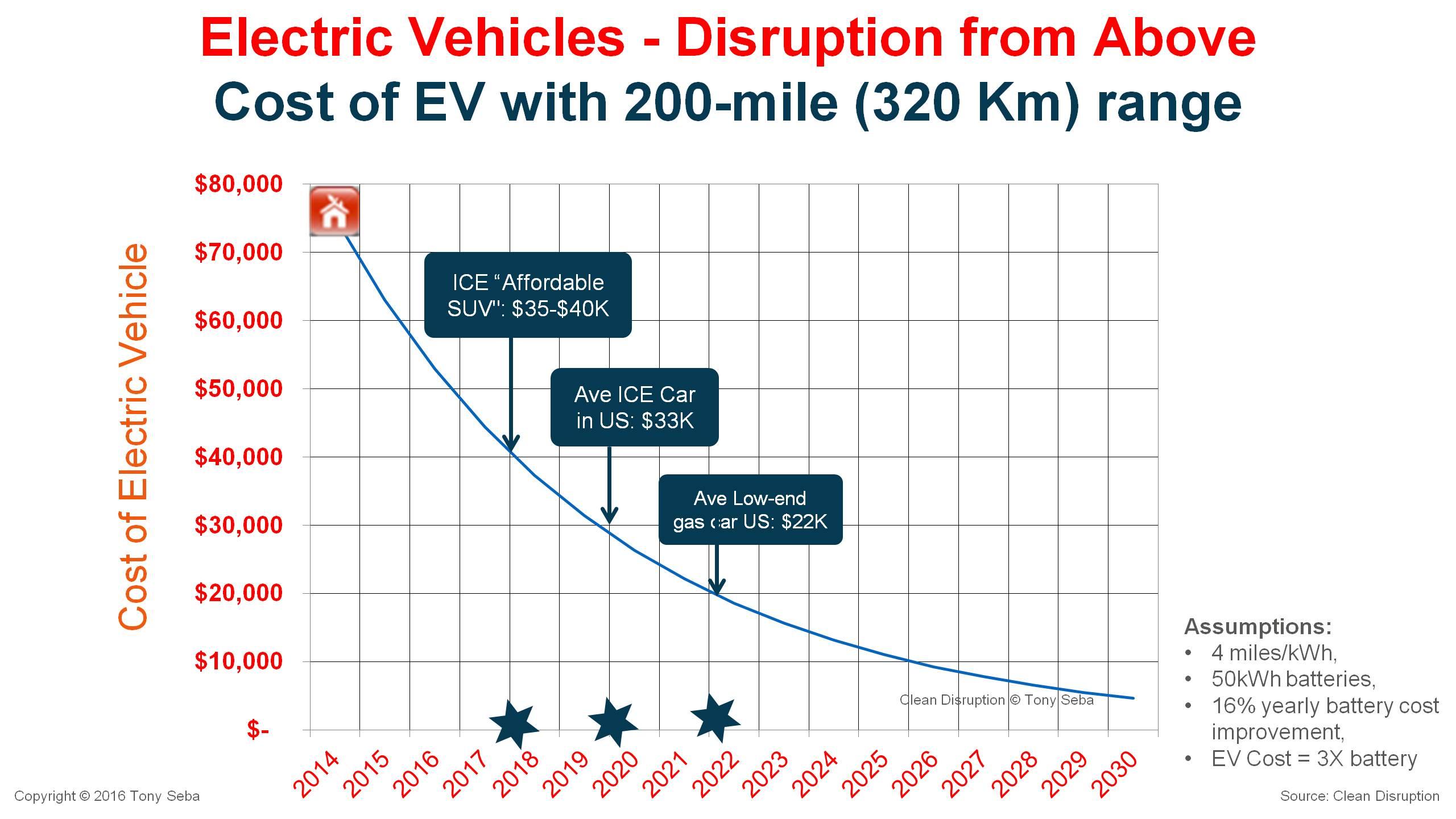

By 2016 Tony Seba was predicting price parity, EV vs ICE, in 2022. (chart) Perhaps Covid threw the timing off but it’s now happening. Throw in maintenance and fuel costs and it’s a no-brainer.

CATL is the future Saudi Aramco or whatever, BYD is the future Toyota or Volkswagen and Tesla is the future … well, they have no comparison. They will have cars/trucks, AI/robotics and energy/utility capabilities.

Mar 13, 2023

SA // hold: BYD Is Still Doing Well After The Expiration Of Subsidies

BYD’s overall global growth percentage isn’t vastly different from their China growth percentage because other segments aren’t yet big enough to move the needle. As such, we shouldn’t expect to see 320% overall growth again but 76% is still very nice.

// GGI 💬

Presuming that 76% growth of sales units is not sustainable long-term, a third of that rate is realistic. If that sales growth is combined with margin expansion, say from the current 5% to closer to 10% for operating income, and the sales outside China become not insignificant (only 2% in 2022) and the FCF keeps piling up (it was -$0.26 in 2019 and in 2022 was $2.16) then stock price appreciation is a very likely outcome.

Feb 7, 2023

SA // hold: World’s Biggest EV Maker Has A Long Road Of Growth

The untapped market is enormous; China’s total NEV fleet was nearly 8 million in 2021 which suggests the country would have roughly around 15 million NEVs at the end of 2022. That is less than 10% of the 302 million total vehicle fleet in China. BYD has numerous competitive advantages to help them capitalize on this opportunity. As China’s leading EV player with a market share of around 30% of China’s EV sales, BYD enjoys strong brand recognition and can clearly stand against global vehicle brands such as Tesla and Volkswagen (OTCPK:VWAGY) (the latter of whom is faltering in China).

// GGI 💬

Fill y’er boots with BYD reviews if ya feel so inclined: https://www.youtube.com/results?search_query=byd+reviews+

https://www.youtube.com/@electricviking/search?query=byd

(Electric Viking even bought himself a BYD Atto 3 for AU$43,000 before fees (US$29,000) and he spends many an hour studying car specs: “handles better than my BMW”, “Tesla better efficiency still better”)

Our first inklings of acknowledgement. And by one of our fave investors:

Absolutely! They are operating directly from Toyota’s playbook in the late 1960s and early 1970s.

— Keith Fitz-Gerald (@fitz_keith) April 14, 2023

{kind=link}