Home Depot » HD // Consumer Discretionary Sector // Strike Price = $xx {subscribe}

NOTE: This report is a Quick Take. We crunched the numbers to come up with a Strike Price. We do not have an in-depth understanding of the products, production capacity, capex, catalysts, risks, markets, competition, moat, management, etc. Buying below our Strike Price could be a reasonable entry point for long-term investors to buy this on sale.

// 🍑 〰️

Who doesn’t love a trip to Home Depot? At least at the beginning of a project. By the fourth trip in your project it gets kinda tedious, but by then you probably know exactly which aisle to hit.

Home Depot is a solid blue chip company with a well established brand moat and pricing power. Management has been getting the job done for decades. The company has dividends and buybacks for shareholders, yellow tag sales for customers and if need be, it seems like a decent place to work at. The company is very much representative of the economy as a whole. Bathroom renos and outdoor living rooms are bought when times are good.

But occasionally that economy can burst its tech bubble (2000), collapse its housing and mortgage markets (2008), or go into chaos-mode from a pandemic (2020). The growth rate of $HD appears to be decreasing but at the right price and including the yield one could outperform the market with this stock. One doesn’t need a huge margin of safety with this stock, as its blue chip-ness should endure, but a margin of safety is still required to protect your downside risk and maximize your upside potential.

// OFFICIAL PROFILE

The Home Depot, Inc. operates as a home improvement retailer. It sells various building materials, home improvement products, lawn and garden products, and décor products, as well as facilities maintenance, repair, and operations products. The company also offers installation services for flooring, water heaters, bath, garage doors, cabinets, cabinet makeovers, countertops, sheds, furnaces and central air systems, and windows. In addition, it provides tool and equipment rental services. The company primarily serves homeowners; and professional renovators/remodelers, general contractors, maintenance professionals, handymen, property managers, and building service contractors, as well as specialty tradesmen, such as electricians, plumbers, and painters. It also sells its products through websites, including homedepot.com; homedepot.ca and homedepot.com.mx; blinds.com, an online site for custom window coverings; and thecompanystore.com, an online site for textiles and décor products, as well as through The Home Depot stores. The Home Depot, Inc. was incorporated in 1978 and is based in Atlanta, Georgia.

// OUR TWO BITS

Apple went public in 1980 at 10 cents per share. IRR through May 31, 2022 with dividends: 19.7%. Home Depot went public in 1981 at four cents. Rate of return with dividends: 29.4%.” Its profitability tops Apple’s. Need I say more?

Ken Langone, Co-Founder and former CEO of Home Depot

// SOME STATS

- Management expect sales growth of 3 – 4% over the long run

- Management target is to open 80 new stores in next 5 years

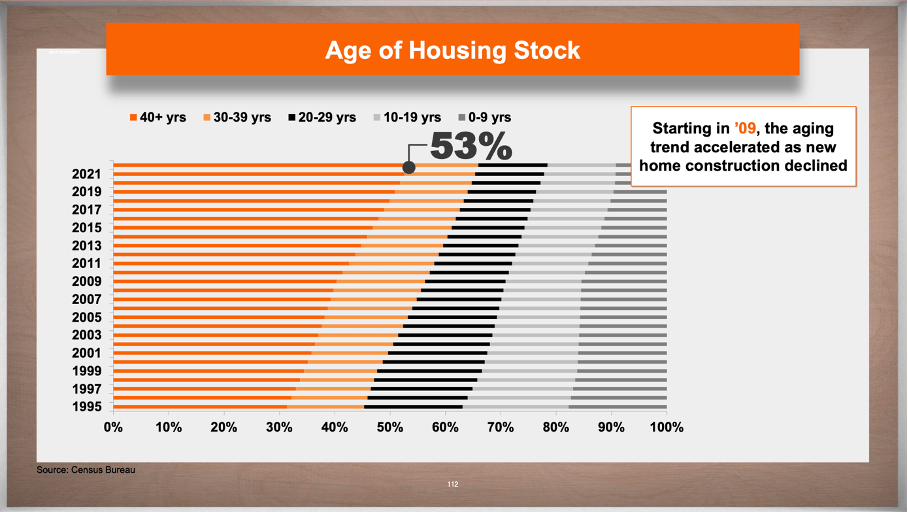

- 53% of houses in USA are now 40 years or older up from about 40% in 2009 🔗

- With over 471K employees it is one of the biggest employers in the country, and it pays about 1% of all taxes paid by corporations in the United States.

// SOME FINANCIAL NUMBERS & ANALYSIS

- 10 year CAGR = 14.8%

- Jul 3, 2013 to 2023 || $77.73 -> $310.02 || high of $420 in Dec 2021

- 5 year CAGR = 9.9%

- 16.7% above 52 week low of $265

- Dividend Yield = 2.7% || $8.36

The bigger it gets the slower the stock price grows as you can see in the 10 vs 5 year CAGRs. The dividend is decent and it has grown at a 16.9% CAGR over the past 10 years. Can they keep that up?

- Future Growth Rate Estimate: xx% {subscribe}

- Previous 5 year EPS = $9.78 to $16.74 for 71.2% growth

- Previous 5 year Revenue = $108.2B to $157.4B for 45.5% growth

- Next 5 year estimates EPS = $14.95 to $19.49 for 30.4% growth

- Next 5 year estimates Revenue = $152.2B to $173B for 13.7% growth

The future growth is expected to be significantly slower than the past 5 years. Will it actually be that bad or is this reflective of analysts using a bearish perspective? There is definitely bearish bias, but between the growth rate and the dividend, we wouldn’t expect significant market out performance (over 10%). But if you can #AbideTheStrikePrice to maximize that CAGR this could be a solid foundational piece to a portfolio.

- 5 year Price Target = $xx {subscribe}

- Price to Sales Revenue multiple = xx {subscribe}

- Sector median P/S (ttm) = 0.9

- currently 2 with a 5 year average of 2.2

They may not grow fast but if they can expand their margins, FCF, dividends and buybacks and market sentiment is positive the multiple could definitely edge higher.

- Price to Free Cash Flow per Share = 24 😀

- Operating Margin = 15% 🤔(but it was -13% Aug 2022)

- Return on Invested Capital = 33.6% 😀

- Long Term Debt to Total Assets = 50% 😢

- Cash & Equivalents to Total Operating Expense = 4.4% 😢

The ROIC of 33.6% is impressive. It means management must be doing something right. But the debt and cash to expenses don’t leave much room for error although numbers like that are part of the nature of the retail business they are in. Profits are being returned to shareholders but bringing debt down and cash up would be nice.

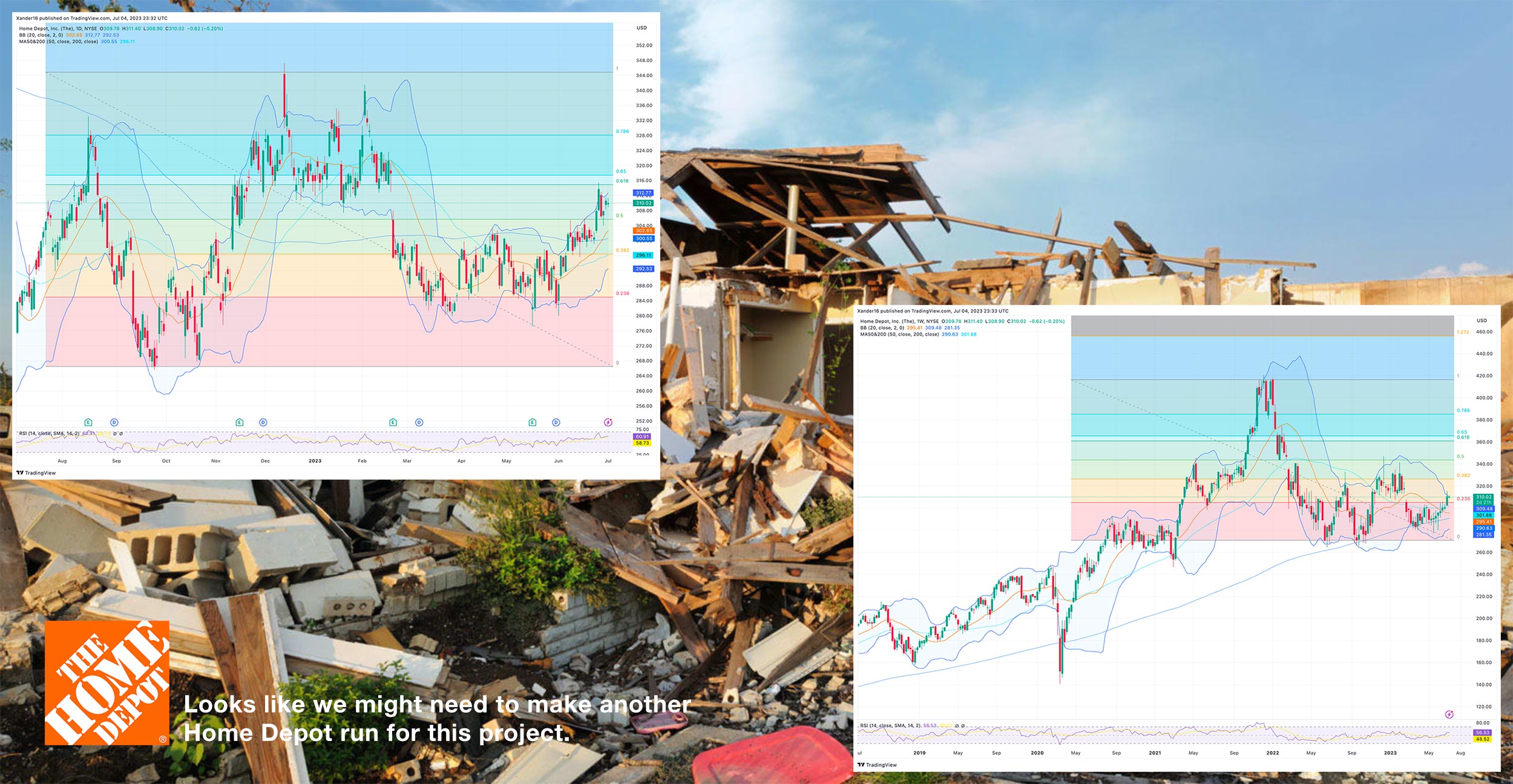

// THE CHART

There is a lot of resistance in the $315 – 45 region but if it can break through that it could run but as blue-chip a company as it is do you see it being valued above intrinsic value like Apple and Microsoft?

// NEWS, REVIEWS & COMMENTS

Seeking Alpha, last 10 articles:

- Strong Buy: 0

- Buy: 5

- Hold: 5

- Sell: 0

All 10 articles written since May 12, 2023.

Jul 1, 2023

SA // buy: Home Depot Can Likely Beat Expectations If Recession Is Avoided

- “Home Depot (HD) is a quintessential blue-chip stock that is currently at a reasonable valuation and has had expectations reduced after COVID demand waned.

- The firm’s proven business, high quality, and exposure to inexorable demographic trends make it a prime candidate for long-term ownership.

- The firm is attractively valued on a relative and intrinsic basis, and the tailwind of strong housing and economic activity creates a good risk/reward for those starting a position.

- There are many risks to the stock, and if recession does occur, then my thesis will be challenged and the price would decline significantly.”

// GGI 💬

Author paints a feel-good story about Home Depot that we mostly agree with. Would still prefer to buy when we find there is a yellow tag sale.

Jun 27, 2023

SA // hold: Trading At Reasonable Valuation Multiples

- “Home Depot performed well in most recessions with the housing crisis in 2007/2008 being the exception.

- The company also had to report declining revenue and earnings per share in the first quarter of fiscal 2023, but only in the single digits.

- While the housing market might be seen as problematic in the next few quarters, renovation of the aging housing stock in the United States might be a tailwind.

- HD stock seems to be fairly valued right now, but is probably not the best investment at this point.”

// GGI 💬

Interest rate increases and inflation and recessions all mean Home Depot sales decrease so the author is right to not throw caution to the wind when valuing the company and its stock.

Green Garage Investing offers a semi-DIY subscription service to help long term oriented investors outperform the stock market index.

- Strike Price List: https://www.patreon.com/greengarage ( < 🍺 per month )

- Newsletter: https://greengarageinvesting.com/newsletter/ ( free weekly )

{kind=link}